The old expression is that money does not grow on trees; you have to work for it. However, if you can find a way, it sure is easier if you can get the government to write you a check out of the treasury.

In short, that is how a TIF (Tax Increment Finance District) works but often times with good intentions.

In short, that is how a TIF (Tax Increment Finance District) works but often times with good intentions.

Back Ground

In 1978, South Dakota was facing a challenge of abandoned and dilapidated areas of previous industry or use that if redeveloped would increase the value of the surrounding tax base and fuel productive economic growth. However, these areas were often embargoed by previous ownership problems, unpaid tax burdens, and derelict buildings that cost more to demolish then they were worth.

As a result, the Legislature defined these areas as blighted see below and brought into existence TIF districts.

As a result, the Legislature defined these areas as blighted see below and brought into existence TIF districts.

How TIFs work

Say you have one city block in town that is no longer in productive use and has potential to be developed in a way that is both advantageous to individuals or companies and the government and the public. In this example, the building of a sports stadium.

Let's use the below numbers in this example:

1. The current city block has a tax assessment value of $1,000

2. The stadium will be worth $101,000 when complete; an increase of $100,000

3. Tax levy is $2/1000.

4. Demolishing the old buildings will cost $20,000

5. The building itself will cost the contractor $90,000 to build.

As a result, if the contractor bought the site, paid for demolition, and built the building, they would have spent $111,000 on a $101,000 building which results in a $10,000 loss.

Beings the blighted area is hurting the surrounding areas, there would be a net gain far in excess of $10,000 to the public if the project was completed. In order to make the project make financial sense, the local government can pay for some of the project cost using money that is repaid (Financed) from future property tax that is gained from the developed property. In this case, the government gives a $3000 TIF to help pay for demolition.

Normally, after the $101,000 building was completed, the county assessor would assess a $202 property tax bill annually on the property that would be paid into the general fund just like the property tax of any surrounding property. Being this is $200 more than the original $2 tax bill, the $200 can be used to pay off

off the $3000 TIF for up to 20 years. With no interest, this would be 15 years at $200/year. With interest paid to the bond holders who paid the original $3,000, say it takes 18 years to pay off.

After 18 years, the TIF is done and all $202 go into the property tax funds which continues long into the future. The increased tax value after the TIF ends makes up for the original investment and the interest paid.

Let's use the below numbers in this example:

1. The current city block has a tax assessment value of $1,000

2. The stadium will be worth $101,000 when complete; an increase of $100,000

3. Tax levy is $2/1000.

4. Demolishing the old buildings will cost $20,000

5. The building itself will cost the contractor $90,000 to build.

As a result, if the contractor bought the site, paid for demolition, and built the building, they would have spent $111,000 on a $101,000 building which results in a $10,000 loss.

Beings the blighted area is hurting the surrounding areas, there would be a net gain far in excess of $10,000 to the public if the project was completed. In order to make the project make financial sense, the local government can pay for some of the project cost using money that is repaid (Financed) from future property tax that is gained from the developed property. In this case, the government gives a $3000 TIF to help pay for demolition.

Normally, after the $101,000 building was completed, the county assessor would assess a $202 property tax bill annually on the property that would be paid into the general fund just like the property tax of any surrounding property. Being this is $200 more than the original $2 tax bill, the $200 can be used to pay off

off the $3000 TIF for up to 20 years. With no interest, this would be 15 years at $200/year. With interest paid to the bond holders who paid the original $3,000, say it takes 18 years to pay off.

After 18 years, the TIF is done and all $202 go into the property tax funds which continues long into the future. The increased tax value after the TIF ends makes up for the original investment and the interest paid.

TIFs Changes in the 1990s and 2000s

During this time, the scope of what type of project could qualify for a TIF was expanded from only blighted areas to any area that will stimulate prosperity though advancement of industrial, commercial, manufacturing agricultural or natural resource development as seen below. In short, in the name of economic development, the scope of potential projects that could be partially paid for through tax dollars was drastically increased.

However, the original 1978 requirement that no residential structures could be paid for still remained as seen below.

Downsides of TIFs

In the example above, the new stadium still requires road to be cleared of snow and maintained just as the neighboring properties do. The stadium also needs Police and Fire Services to be ready to respond to emergencies just as neighboring properties do. However, until the TIF ends, only the original $2 of property tax revenue is available to support these needs as the new $200 of taxes are predetermined to be used on paying down the bonds that paid for the $3,000 demolition plus interest. This shifts the tax burden onto all other properties in the county temporarily.

In short, while the property IS paying property tax on the full new value of $101,000, the vast majority of those taxed never make it to the treasury but are instead paid back to repay the original project costs. If the owner of the property had their original project subsidized by a TIF, they are essentially paying back a loan to themselves at a rate equal to what their increased property tax bill would have been.

Additionally, the terms and interest rate of the bonds issued to pay for the TIF are only determined by the governing body and NOT subject to a vote of the people per the state law below.

In short, while the property IS paying property tax on the full new value of $101,000, the vast majority of those taxed never make it to the treasury but are instead paid back to repay the original project costs. If the owner of the property had their original project subsidized by a TIF, they are essentially paying back a loan to themselves at a rate equal to what their increased property tax bill would have been.

Additionally, the terms and interest rate of the bonds issued to pay for the TIF are only determined by the governing body and NOT subject to a vote of the people per the state law below.

Where Sioux Falls Is Trying To Take TIFs

East Ridge District (TIF #26) is a proposed affordable housing development consisting of 9.7 acres in northeast Sioux Falls that will be built out into 65 "first time new home buyer" homes that will be priced at 60% to 100% of South Dakota Housing Authority First Time Home Buyer Pricing. In short, these homes are to be sold at a market price that without a government subsidy would not be profitable to the developer, in this case Nielson Development, LLC.

The planning agency has stated that they cannot use tax dollars to pay for the building of the homes directly; they interpret SD 11-9-42 to allow them pay for site work on the ground currently owned by Nielson Development that will then have strictly residential structures built on that improved ground by Nielson Development that will then be sold by Nielson Development at a profit. For up to the next 20 years, the estimated property tax increment of $300,000 will be used to pay back the $2.14 million cost of site development plus interest that the city of Sioux Falls paid to lower the cost for Nielson Development, totaling up to $6 million of tax revenue that will be diverted to pay for the original TIF.

The planning agency has stated that they cannot use tax dollars to pay for the building of the homes directly; they interpret SD 11-9-42 to allow them pay for site work on the ground currently owned by Nielson Development that will then have strictly residential structures built on that improved ground by Nielson Development that will then be sold by Nielson Development at a profit. For up to the next 20 years, the estimated property tax increment of $300,000 will be used to pay back the $2.14 million cost of site development plus interest that the city of Sioux Falls paid to lower the cost for Nielson Development, totaling up to $6 million of tax revenue that will be diverted to pay for the original TIF.

How This Is Statutorily Illegal

1. To think that paying for site preparation work on ground that will exclusively be used to build houses is NOT using TIF funds for construction of residential structures is fool hardy at best. Without the above-mentioned site work, the current corn field would not support building of these houses. As a result, the site work is part and parcel to the construction of these residential structures.

On this statue SD11-9-42 alone, this entire effort is illegal.

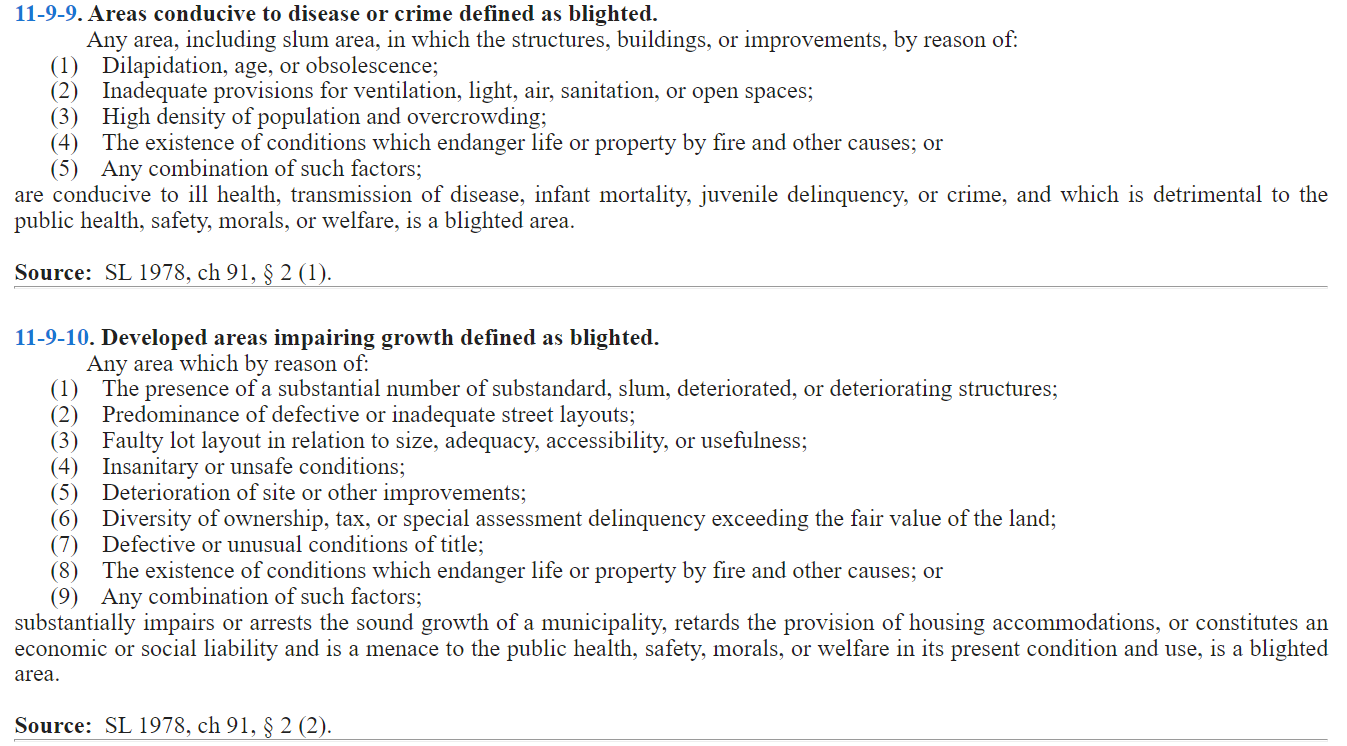

2. Statue SD 11-9-8 puts forward a test of if an area qualifies for a TIF.

A. 25% of the area that is in the TIF district is defined as blighted per the 1978 original intent of the program.

Answer: In no way is does contiguous parcel of productive ag land in a prime development site qualify as blighted so this cannot authorize the project.

B. 50% of the area will paraphrase "promote economic prosperity through advancing industrial, commercial, manufacturing, agricultural, or natural resource development."

Answer: 0% of the area completes these tasks as 100% of the area is devoted to exclusively residential housing. This test cannot authorize the project.

As none of the above methods can authorize the project to use TIF funding, to make this be a TIF district would be illegal.

On this statue SD11-9-42 alone, this entire effort is illegal.

2. Statue SD 11-9-8 puts forward a test of if an area qualifies for a TIF.

A. 25% of the area that is in the TIF district is defined as blighted per the 1978 original intent of the program.

Answer: In no way is does contiguous parcel of productive ag land in a prime development site qualify as blighted so this cannot authorize the project.

B. 50% of the area will paraphrase "promote economic prosperity through advancing industrial, commercial, manufacturing, agricultural, or natural resource development."

Answer: 0% of the area completes these tasks as 100% of the area is devoted to exclusively residential housing. This test cannot authorize the project.

As none of the above methods can authorize the project to use TIF funding, to make this be a TIF district would be illegal.

School District Funding Shortfalls

Historically, when TIF Districts were used, the short-term diversion of property tax revenue from the normal property tax fund budgets was viewed as a reasonable tradeoff for the removal of the societal harms of the blighted area and the long-term benefits of the increased property tax revenue after the TIF was dissolved.

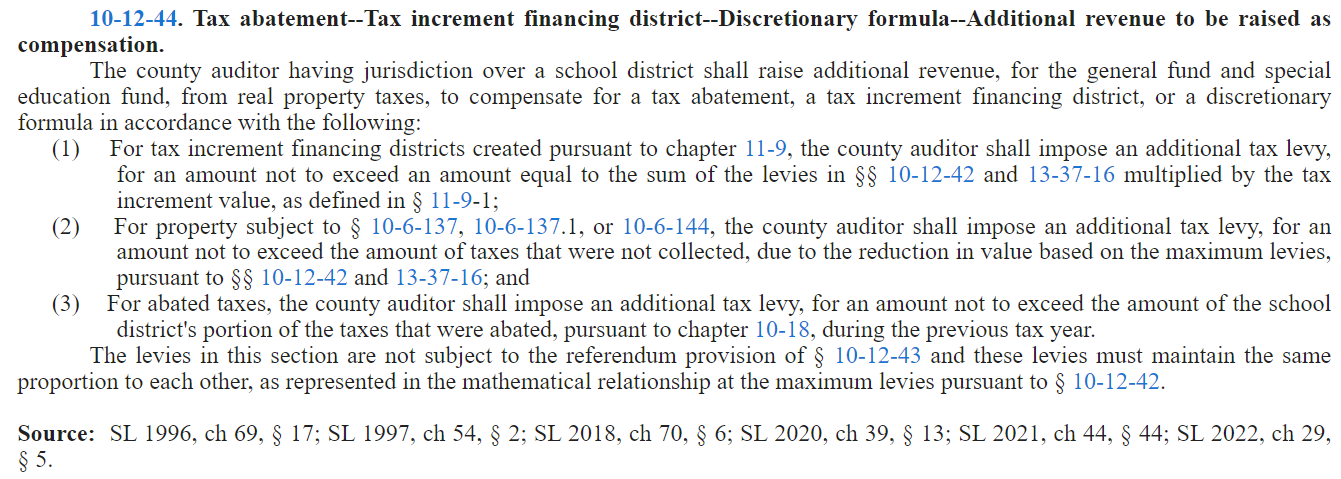

However, local school districts could not wait up to 20 years for the future increase in funding that was needed to educate the children today. As a result, section 1 was included in SD 10-24-44 which forced to county auditor to place additional tax burden on TIF properties to generate the equivalent level of general fund revenue to make the school districts general funds whole.

However, local school districts could not wait up to 20 years for the future increase in funding that was needed to educate the children today. As a result, section 1 was included in SD 10-24-44 which forced to county auditor to place additional tax burden on TIF properties to generate the equivalent level of general fund revenue to make the school districts general funds whole.

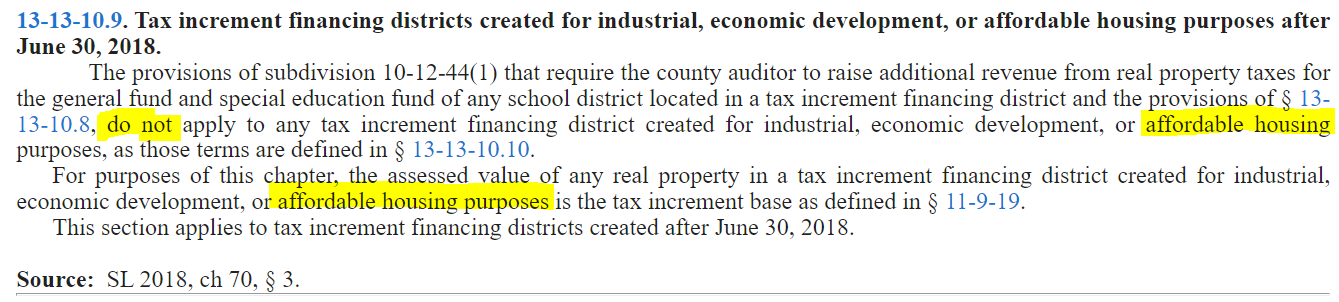

However, as this TIF effort is being classified as an affordable housing TIF, these additional fees will not be assessed to these residential structures due the 2018 law that created SD 13-13-10.9

As a result, these additional fees will not be levied on these residential structures. This will force the "local effort" of the state aid to education formula to remain constant as children move into these new homes. The general fund of the Brandon Valley school district will subsequently be increased by ~$6,600 per child using state general funds evenly distributing this increased tax burden across all South Dakota taxpayers.

As a result, these additional fees will not be levied on these residential structures. This will force the "local effort" of the state aid to education formula to remain constant as children move into these new homes. The general fund of the Brandon Valley school district will subsequently be increased by ~$6,600 per child using state general funds evenly distributing this increased tax burden across all South Dakota taxpayers.

Increased School District Funding Challenges

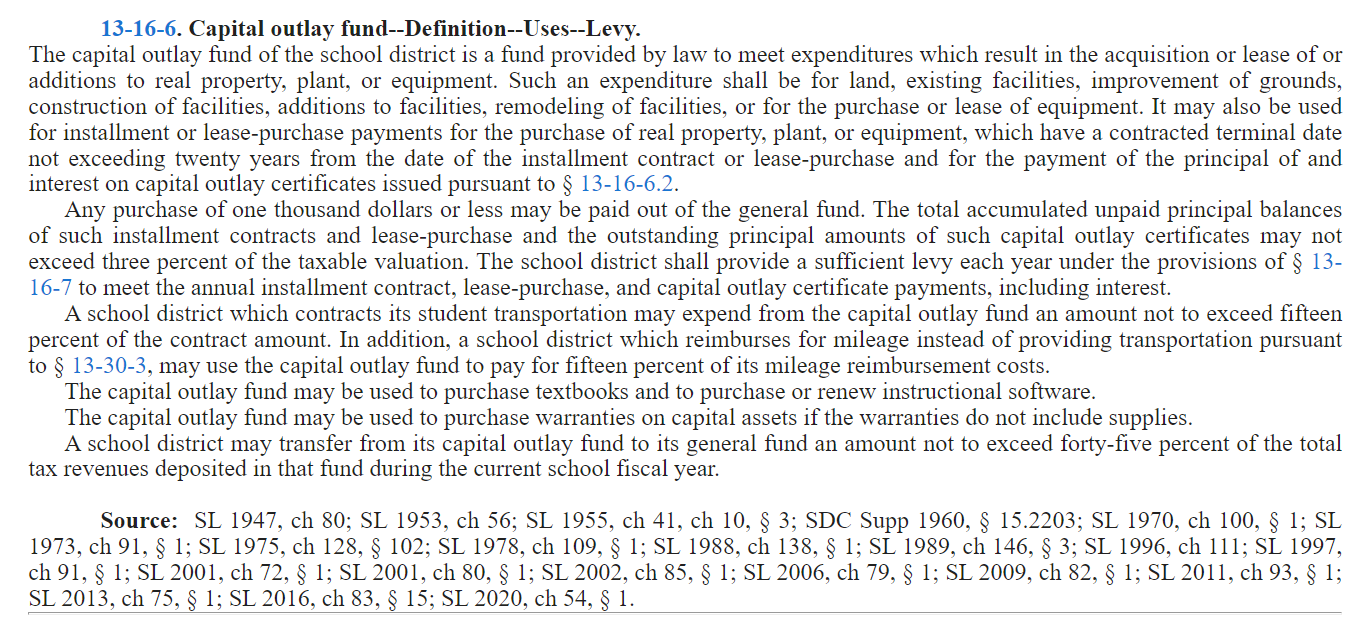

Beyond shifting the local general fund tax burden away from the residents of these homes, the capital outlay fund as described in SD 13-16-6 of the Brandon Valley school district will not have any taxable exposure to these properties for 15 years.

Therefore, as residents and children move into this development, the need for classroom space and textbooks will increase but there will be no funding mechanism to provide for those needs.

If passed, the City Council of Sioux Falls will be paying Nielson Construction to install streets and sewers today exclusively for houses for children in the Brandon Valley school district using the financial resources that are intended to purchase their textbooks for the next 15 years plus 5.2% annual interest, all with no vote of the affected school district or the state residents as a whole.

Therefore, as residents and children move into this development, the need for classroom space and textbooks will increase but there will be no funding mechanism to provide for those needs.

If passed, the City Council of Sioux Falls will be paying Nielson Construction to install streets and sewers today exclusively for houses for children in the Brandon Valley school district using the financial resources that are intended to purchase their textbooks for the next 15 years plus 5.2% annual interest, all with no vote of the affected school district or the state residents as a whole.